Did you know that nearly 60% of homes in the U.S. are underinsured against disasters? It's time to rethink how we protect our assets. This isn't just a matter of financial security—it's a call to action that can't wait.

With climate changes causing more frequent and severe natural disasters, the necessity for adequate disaster insurance has skyrocketed. Homeowners who felt secure just a decade ago are now at high risk, financially unshielded against these unpredictable events.

Consider this: while millions assume their standard policies are enough to cover every crisis, most are stunningly mistaken. Disasters like hurricanes, floods, and wildfires require specialized insurance that significantly differs from regular policies. But that’s not even the wildest part…

Another shocking truth? Many insurance companies have clauses that exclude several common catastrophes unless explicitly stated. Homeowners often discover these gaps only after tragedy strikes. But what other blind spots might be lurking in your coverage? Well, this piece isn’t done revealing its secrets just yet.

What happens next shocked even the experts—unveiling a hidden network of coverage loopholes and strategies you must adopt next. Are you truly protected, or merely paying for peace of mind that doesn’t exist? Stay tuned.

Most homeowners rely on standard insurance policies believing they're comprehensive, but these plans can be riddled with exclusions. For instance, while fire damage is typically covered, you might be surprised to find other disasters, like earthquakes and floods, are often omitted. This misconception leaves countless homes vulnerable when calamity strikes.

Industry insiders reveal that many insurers prioritize profit, sometimes leading to policies that barely scratch the surface of real coverage needs. The tricky part is that these loopholes are buried in technical jargon, making it challenging for average policyholders to decipher. But there’s one more twist…

To protect yourself effectively, it’s crucial to assess your geographical risk factors. Areas prone to specific disasters might require separate insurance policies—such as flood or earthquake insurance. Interestingly, some advanced tools, like risk assessment software, can help evaluate your home’s vulnerability and suggest needed coverages. What you read next might change how you see this forever.

But here lies the heart of the issue: a significant percentage of homeowners don’t review their insurance until it’s too late. This ignorance can lead to devastating financial losses. Next up, we’ll dive into strategies to overhaul your coverage and safeguard your assets more effectively. It’s time to reconsider what insurance means for you in today’s perilous world.

Beyond the obvious damage from natural disasters, hidden costs can pile up quickly. For example, even if your home insurance covers structural damage, what about the interim living expenses while your house is repaired? These unexpected bills can compound, straining finances further.

Consider costs like debris removal and secondary damages, such as mold resulting from water infiltration. Many policies provide coverage for these—but often, the coverage is capped at a low amount. Plus, not all types of mold damage are considered equal under policy terms. As you delve into the details, the complexity increases.

Some homeowners assume that their policy's coverage limits automatically adjust with inflation and property value increases, but this isn't always true. Many plans require annual reviews and adjustments to ensure adequate protection. The lesson? Regular policy evaluation is more crucial than it seems.

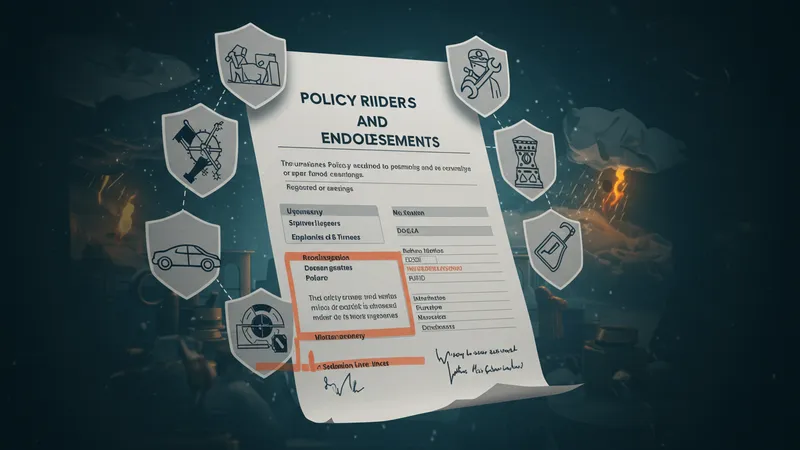

The next segment will dissect the elusive concept of policy riders—additional coverages tailored to plug those overlooked gaps. These can include invaluable protections like increased rebuilding costs or bespoke protection for high-value items. Knowing this could save you thousands, if not more. Ready to uncover more?

Policy riders, often perceived as mere add-ons, can actually serve as powerful tools to enhance your disaster insurance. These optional extensions tailor your policy to exceed basic constraints, addressing unique risks that standard policies ignore.

For instance, should you own pricey collectibles or a luxury vehicle, a rider can ensure they're covered for the full value. Additionally, reconstruction costs have climbed substantially due to material shortages, necessitating a review of your maximum payouts.

Endorsements, another vital element, alter the policy terms, offering flexibility and personalized protection. By leveraging both riders and endorsements, you can bridge coverage gaps. But not all insurers extend these add-ons, making it essential to shop around for the best options.

Mastering these components empowers you to construct a policy that genuinely caters to your needs. But before finalizing anything, there's another critical factor to consider—the role of deductibles and their impact on premiums. Curious? Let’s dive deeper.

Deductibles are a double-edged sword in insurance policies. While raising them can reduce premiums, it also means higher out-of-pocket costs when disaster strikes. Striking the right balance is crucial to ensure that you're not financially overwhelmed during a crisis.

However, there's more than meets the eye. Deductibles apply differently across various types of claims. Floods or earthquakes often come with different—and sometimes higher—deductibles compared to other types of damage. Ignoring these variations can lead to unexpected financial strain.

Furthermore, opting for a high deductible might lower your initial costs, but when facing a major claim, the financial toll can be severe. It’s imperative to evaluate your fiscal capacity to cover a deductible in an emergency without destabilizing your finances.

Take charge by consulting with your insurance agent to customize a deductible that aligns with your risk tolerance. But remember, there’s another pivotal piece of the puzzle—the timing of policy claims. Get ready to uncover why timing is everything in the next section.

Making strategic decisions about when to file a claim can significantly impact your insurance benefits. Timing can influence your premiums and even availability of future coverage. Not every incident warrants an immediate claim, especially if it could raise your rates.

Some seasoned policyholders choose to cover minor repairs out-of-pocket, reserving claims for major damages. Insurers sometimes penalize frequent claims with increased premiums or, worse, non-renewal notices. But the urgency of severe disasters can compel instant claims that are non-negotiable.

Understanding the ideal timing involves a delicate balance between immediate need and long-term cost effectiveness. Consulting with an insurance advisor before making decisions can help navigate these waters cleverly, ensuring you're covered when it truly matters without incurring lifelong premium hikes.

But there's a twist—not all claims are treated equally. Knowing the insurer’s specific assessment criteria can give you an edge in securing a fair settlement. What factors influence this? That’s precisely what we’ll explore next.

Insurance claim settlements are not always transparent. Various factors play into the final payout, such as the thoroughness of your original documentation and the perceived credibility of your claim. Knowing this can be the difference between a smooth claim and a drawn-out battle.

Some policyholders find themselves unexpectedly low-balled because they didn’t capture enough proof at the scene of the disaster. High-quality images and itemized inventories can act as strong evidence, bolstering your case. Expert advice suggests keeping an annual update of these records to align with policy changes.

Moreover, negotiating skills can come into play. Engaging with experienced claims adjusters or even hiring a public adjuster can tilt the scales in your favor, ensuring you get the compensation you deserve. But even then, insurers often have a few tactics up their sleeve.

One more thing you must know—appealing a claim decision. This procedure is rarely straightforward but can be indispensable when faced with unfair settlements. How can you effectively challenge a decision? Stick around as we delve into that next.

Faced with a disappointing insurance payout? Rest assured, you can appeal for a reconsideration. It’s a route many overlook, assuming initial decisions are final. However, a strong appeal rooted in evidence can shift insurer decisions significantly.

Begin by thoroughly reviewing your policy’s terms and the claim denial notice to understand the justification. Often, policies have specific steps outlined for appeals, and adhering to these processes is crucial. Accurate, organized documentation serves as your strongest ally in these cases.

Consulting legal advice or contacting a public insurance adjuster can provide additional leverage, presenting your case in the most compelling manner possible. Remember, this isn’t just about statistics and paperwork. It's about persistence and showcasing the reality of your loss.

But there’s a catch—statutes of limitation on appeals vary by jurisdiction. Missing a filing deadline can forfeit your rights entirely, so timing is everything. Ready to learn what industry experts use to safeguard their holdings? Let's explore that in the following section.

Industry insiders champion the practice of bundling policies to secure broader and often more affordable coverage. For example, combining home, auto, and umbrella insurance can lead to significant discounts, thus amplifying your financial safety net.

Moreover, a growing trend among savvy policyholders is leveraging technology. Smart home devices can significantly reduce risks, and insurers often reward their installation with reduced premiums. Monitoring these trends keeps your approach up-to-date with industry best practices.

Regular policy audits, suggested at least once a year, help identify new risks and adjust coverage limits accordingly. Taking a proactive stance prevents devastating losses in the face of evolving disaster threats. Insurers are more accommodating when they see a policyholder actively managing their risk.

What the experts emphasize, however, is the significance of transparent communication with your insurance agent. This ensures clarity and adequacy in coverage, so no unexpected gaps arise when calamity hits. There’s one aspect we’ve yet to unveil—what happens if you face uninsured losses? Keep reading, discovery awaits.

Uninsured losses can be financially catastrophic, leaving you scrambling for a solution. But there are options. Relief may come from disaster relief grants or loans offered by government programs designed to assist those who’ve slipped through the insurance net.

Community resources, such as non-profit organizations, often extend aid to help rebuild. Additionally, crowdfunding has become a modern salvation for some, enabling friends, family, and strangers to contribute towards building back what's lost.

Forging a recovery path requires creativity and patience. Experts advise ranking your financial priorities to effectively manage resources. It's a balancing act of fulfilling immediate needs while planning for long-term stability—a daunting but necessary strategy.

The next pressing issue? How to prevent future gaps in coverage. Strategies abound, and proactively integrating them can determine resilience for decades to come. Get ready to dive into preventative practices that fortify your future against uninsured disasters.

An ounce of prevention is worth a pound of cure, as the saying goes. Tailoring policies with specific attention to known local hazards is a foundational step in proactive coverage management. Understanding the historical risks in your area can highlight potential future threats.

Routine maintenance and updates to your dwelling can qualify you for discounts and reduce claim likelihoods. Upgraded roofing and reinforced windows, for example, can withstand stronger storms and may decrease insurance costs.

Engage your insurer actively, scheduling regular reviews to account for shifts in climate patterns or changes in personal circumstances that could affect risk. Staying informed about upcoming climate threats and adaptation strategies ensures nothing takes you by surprise.

Predictive risk management technology is rapidly advancing. Some organizations offer free assessments to pinpoint vulnerable areas in your insurance and physical property. This foresight could forestall tragedy. But what profound revelations await in our final chapter?

As weather patterns grow more erratic, the entire insurance industry is evolving at breakneck speed. Some firms are investing in climate science to better ascertain risk factors, yet others face criticism for denying coverage based on predictive models alone.

Blockchain technology and smart contracts are emerging as transformative forces, promising faster claims processing and unalterable records. These advancements could lead to unparalleled transparency—a potential industry game-changer.

Furthermore, disaster insurance is increasingly not just about individuals, but communities. Shared policies or community risk pools are becoming viable options, spreading risk and cost more equitably among neighbors.

This burgeoning frontier of insurance implies a radically different landscape in a few short years. Navigating these changes with informed vigilance could be the key to sustainable security. But there's one last takeaway that ties it all together—prepare yourself for an astonishing wrap-up.

Our deep dive into disaster insurance reveals a stark reality: protection doesn’t happen by accident. As unpredictable as disasters are, our approach to safeguarding assets must be proactive, informed, and adaptable. By embracing technology, scrutinizing policies, and cultivating a habit of vigilance, we can shield our future from the unforeseeable.

Share these insights with someone you care about or revisit them as your circumstances change—being prepared is the first step towards peace of mind. Now it's time not only to protect but to empower and inform others through actionable insights!